4 minute read

Capitalizing on the expanding global commercial card market

The commercial card market is experiencing rapid growth and significant transformation, driven by fintech entrants, new solutions and changing client needs and expectations.

Spend with global commercial cards — including debit, credit, prepaid and virtual cards — exceeded $4 trillion for the first time in 2023, reflecting a growing business reliance on commercial cards for strategic expense management during times of economic uncertainty.

With global spend projected to exceed $6 trillion by 2029, commercial card usage is moving beyond traditional travel and expense purposes into areas such as software subscriptions, field operations, logistics and supplier payments. Small and medium-sized businesses (SMBs) are seeking new ways to streamline supply chain management and reduce reliance on manual payment methods.

SMBs are increasingly replacing account-to-account (A2A) bank transfers and cheques with commercial cards to better monitor payments, drive further cost efficiencies and manage cash flow. Corporates are similarly driven by enterprise cost control and a desire for a centralized payments approach across growing spend categories.

There is also the need for greater digitization and automation of business-to-business (B2B) payments. In this space, virtual cards are proving to be a significant change agent for driving improvement in efficiency and user experience, with benefits including heightened security, reduced fraud and improved real-time data for automated reconciliation.

“Virtual cards turn payments into a strategic advantage by helping businesses spend smarter and focus on what really matters,” said Javid Moosaji, B2B Business Development Lead, FIS Total Issuing™ Solutions.

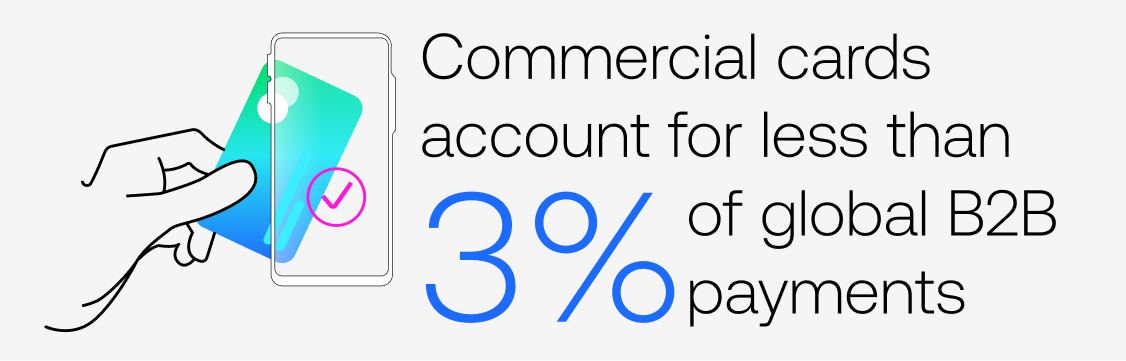

Despite the potential of commercial cards, they account for less than 3% of global B2B payments.

How can issuers tap into a market that is predicted to reach $124 trillion by 2028? By addressing the historical concerns around commercial cards and delivering a winning value proposition for SMBs and corporates.

Defining the business case

Historically, several barriers have stood in the way of businesses utilizing commercial card programs. These include limited supplier acceptance, laborious application processes due to issuing bank know your customer (KYC) and anti-money laundering (AML) policies, and a resistance to change. Additionally, lack of interoperability of business platforms and manual intervention have hindered adoption.

Interoperability is paramount to ensuring that the abundance of data from different endpoints can be channeled to support transformational benefits for SMBs and large companies.

Issuers can help address these barriers through educating their clients about the benefits of commercial card solutions, including the cost of manual payments and reconciliation.

According to Ardent Partners, the cost of manual invoice processing can be about $10 on average per invoice, taking into account employee time for data entry and approvals, physical storage and errors that require manual correction. The real cost is often higher due to hidden expenses like delayed payments, penalties and lost productivity. In this context, automation can play a transformational role. Particularly when using new and emerging technologies to automate traditional manual processes.

With cardholder authentication, for example, combining AI and biometric technologies to combat fraud can bolster the commercial card proposition and cardholder experience — a topic that was discussed at the recent 2025 Commercial Payments International Summit.

SMB benefits

With commercial cards, SMBs can gain significant efficiencies in overhauling time-consuming and error-prone manual reconciliation processes.

In addition, commercial cards may also protect and strengthen cash flow and working capital management by providing better data visibility and customizable spending controls, as well as extending days payable outstanding for buyers while allowing them to pay suppliers sooner.

Commercial card payments are also guaranteed, unlike checks or A2A, which can bounce or be reversed. As such, SMBs could use guaranteed payment through commercial cards to negotiate better supplier terms. Plus, leveraging a commercial credit card’s extended payment terms is particularly critical in this economic environment as SMBs often struggle to access bank loans or credit lines.

Advantages for corporates

For corporates, commercial cards could offer greater control and transparency with transactions. Single-purpose virtual cards, for example, are well positioned for digital spend and evolving customer experiences across all functional areas, whilst offering a strong defense mechanism against continuously changing fraud attacks.

Additionally, corporate cards combined with carbon calculator capabilities can also present corporates with helpful sustainability reporting solutions on card-based transactions. This is particularly important at a time when environmental, social and governance (ESG) goals and initiatives are elevated to the top of many corporate strategic agendas.

“The real-time integration of payment and card data with sustainable-driven innovation to support ESG reporting and corporate transparency was discussed during our recent Commercial Cards Roundtable at MoneyLIVE Nordic Banking. For example, sustainability-as-a-service offerings with carbon footprint trackers provide a significant opportunity to analyze detailed spend data, measure CO2 impact and turn the data into actionable insights, towards a more sustainable future,” said Moosaji.

Throughout the B2B payments space, policy compliance and reporting obligations could be made easier through automated approvals. Modern commercial card solutions enable a holistic view with real-time monitoring along with inbuilt controls to allow businesses to positively reduce their manual efforts and shift investments to their core operations.

Issuer strategy

As SMBs and corporates continue to digitize their B2B payment flows, augmenting commercial card solutions with other emerging payments products could be key.

One potential result of issuers offering alternative card payment options to their customers is improving retention rates.

In addition, commercial cards — particularly virtual cards — support the trend toward embedded finance, in which issuers can embed commercial card payments into their existing front-end mobile and web experience to support greater digital payment options.

“Virtual cards help SMBs feel in control of every purchase without extra admin weighing them down. For large corporations, virtual cards unlock scalable automation and deep spending visibility across complex operations. Plus, virtual cards reduce risk with built-in security and real-time controls,” said Moosaji.

One key to success for commercial card issuers, is working out how to help corporates and SMBs implement card programs in the most cost-effective and seamless way.

Once an issuer has refined its commercial card value proposition, it should determine if it has the right infrastructure to offer the capabilities and features needed for an optimal customer experience.

Issuers might be constrained by platforms built with only consumers in mind. This limits flexibility for business hierarchies and additional commercial card data, which could restrict the overall agility of the commercial card offering. A legacy technology stack can also hold back an issuer and is costly to manage.

Issuers can better manage their technical debt by outsourcing the core processing to a modern payment platform such as FIS Total Issuing™ Solutions, which has a single platform solution tailored for both commercial and consumer products, as well as value-added services such as fraud and risk management, expense management, rewards, real-time data streaming, real-time alerts, API-enabled controls and rich integration options.

Latest articles

Never Miss an Insight

Get the latest from TSYS a Global Payments Company